If you don’t have individual or group medical and dental insurance, medical bills can go up quickly. The provincial plan OHIP does not cover many medical services, such as dental treatment, massage, vision, hearing, etc. So one has to pay out-of-pocket if required and buy a private medical and dental insurance plan.

How much medical and dental insurance costs?

According to a Monster Job Board survey, Canadians spend about $2,000 on medical, and about $4,000 on medical and dental. Fortunately, many companies offer medical and dental benefits to their employees. These are called benefits, and benefits help keep workers for a long time.

Let’s look at the frequently asked questions of medical and dental insurance plans.

There are two types of health and dental insurance plans.

Individual medical/health and dental insurance plans – As the name itself specifies, individual plans are for single or family. Individual plans are more expensive than group plans, but not from the annual health and dental treatment cost.

Group plans – Some companies offer on job benefits, called group health and dental insurance plans. Group plans are cheaper than individual plans, and medical underwriting is comparatively easier.

We have individual, family and group plans available, does not matter if you are looking for Manulife health and dental, SunLife health and dental insurance, green shield health and dental plan, or any other provider, we have all companies at the cheapest prices. Contact us today, let’s design the best health and dental insurance plan as per your needs.

Does the provincial healthcare cover dental treatment?

No, they do not cover dental treatment under provincial health care in most provinces of Canada. However, depending upon circumstances, limited coverage is available for low income Canadians.

Can we get dental treatment for free?

Yes, there are programs available in Ontario, such as healthy smiles, but available for a few families, those meet certain requirements. Otherwise, dental treatment is not free.

Is Health and Dental Insurance Necessary?

Insurance is a security, more coverage, better security. According to data from Monster Job Board, annually, an average Canadian spends $2000 on dental and $4000 on health and dental plan, which is way more than the cost of health and dental insurance.

Are you looking for an individual health and dental plan? We got a no obligation quote for you.

A RESP Child Plan is the best way to invest in your child’s educational future

The Registered Education Savings Plan is offered by the government of Canada for the purpose of saving for your child’s higher education. With this tax-advantaged plan and a grant from the government of Canada, you can save enough to pay for college fees.

What are the benefits of RESP?

Main benefits of RESP are

Tax-sheltered growth.

A RESP account is a tax-free account, so the growth is tax-free. Withdrawals are taxable, but since your child’s income falls into a lower bracket, the taxes are minor.

Government Grant.

In addition to what you contribute, the government also puts extra money into it, which contributes to growth. Nevertheless, expert advice can help you to find out how much your child will receive as a government grant.

Provider Bonus or growth.

Money invested in RESPs grows faster than traditional investments.

Funds can be used for all educational purposes.

You can use the accumulated funds for full-time education, part-time education, or any other mode of learning.

It is hard to pool money without RESP

Even though it is difficult to save money, RESPs are not big investments, giving you the opportunity to deposit small amounts on a regular basis.

How many types of RESP, Child plans are there?

The RESP, registered education savings plan can be categorized into three types.

Individual RESP – As the name specifies, the individual RESP is for single beneficiaries.

Family RESP – A family RESP is for more than one beneficiary, in other words, a plan for two or more children. Each beneficiary has access to the entire amount accumulated.

Group RESP – Is for one beneficiary, but there may be more than one contributor. Multiple family members can contribute to one RESP and save for one child.

Can RESP be transferred?

If your child does not wish to pursue higher education, you may transfer the RESP to another child.

Is there any limit on RESP contribution?

A lifetime RESP contribution limit is $50,000, but there is no annual contribution limit on RESPs. Contribute about $2500 a year to maximize your CSEG.

RESP age limit

You can contribute to an RESP, registered education savings plan for up to 31 years. However, the CSEG is up to 18 years.

What is the RESP withdrawal limit?

There is no cap on withdrawals for PSE (Post-Secondary Education). Withdrawals from the EAP (Education Assistance Payment) are limited to $5000 for full-time and $2500 for part-time students.

Is RESP a great idea?

Yes, a RESP is the best investment for your child. Let us help you fulfill your child’s education dreams today.

Wana to save for your kids education today? Use our RESP Calculator tool and find out how much you can save. Or contact us for further assistance

Why is Medical Insurance for Truck Drivers is Required?

First, the Canadian provincial health plans do not cover medical care outside of the provinces or provide limited coverage outside of the provinces. Nevertheless, most of truckers drive across Canada or to the USA.

In addition, if a trucker is involved in an accident outside of the home province, particularly outside Ontario, one might have to pay the hospital bills out of pocket. So,this could result their family may face financial hardhsip.

A third reason is that trucking is a hard job, prone to hazardous situations, because it involves being on the road, dealing with inclement weather, and working long hours.

Finally, you need insurance to support your family, since expenses, mortgages, and bills continue even if you cannot work.

Which medical insurance is good for truck drivers?

Insurance bundles that cover travel, accidental death, dismemberment, disability, soft tissue, and illness are the ideal for truckers. Besides these add-ons and benefits, some insurance companies also offer extras, such as health benefit plans in group policies.

Optional Add-ons in medical insurance for truckers bundle

Illness Cover– In trucking, especially long haul drivers, are prone to illnesses, because of cab shivering and plastic interiors. So, the illness coverage is not pinching, it is worth it to save your enterprise.

Total Disability– A lump sum payment plans are also available and it can be a top up in the package, one time paid out and offered by most disability insurance companies.

Even more addons such as lifestyle protection enhancer, health and dental benefit plans, and family coverage plans are also available in the market.

Almost everyone is eligible for a trucker insurance package, with a valid status in Canada.

An experienced insurance advisor can help you choose the right medical insurance plan. We specialize in Truck Driver Medical Insurance, and work with all major insurance companies.

Individual vs group emergency medical insurance for truck drivers.

For trucking companies, group plans are cheaper than individual plans. You can get a great discount if you have over 20 drivers and the discount increases with the number of drivers. Talk to our expert about emergency medical insurance for trucking companies. We have already designed a lot of plans. Now let’s start yours.

Things to keep in mind when buying emergency medical insurance for a truck driver.

– Always buy a multi trip plan. – Make sure that you buy disability insurance based on your income, because the benefits are based on it. – Buy the right insurance. If you already have a policy, let us review it for you. – Prefer a policy with 24-hour coverage, as it will provide coverage in the event of an accident outside the truck.

The following are the basic components of every coverage.

– 5 million emergency hospital coverage. – 24 hour support. – Hospital food and accommodation. – Ambulance call. – Lab tests. – Prescription medicines. – Healthcare equipment. – Unlimited trips. – Return home in case of an emergency. – Emergency air travel. – Travel of companion to the home. – Return of the vehicle home. – Emergency dental treatment.

Buy online now, Click on the Edge Express Quote.

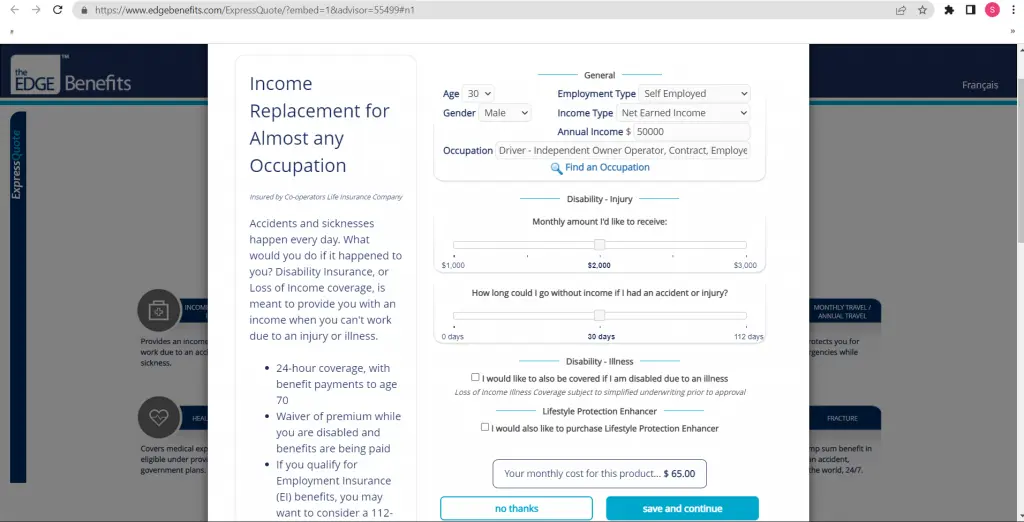

Now, it opens up in a new browser(make sure pop-ups are not blocked). Click on the “INCOME REPLACEMENT BENEFITS” as pointed in the picture.

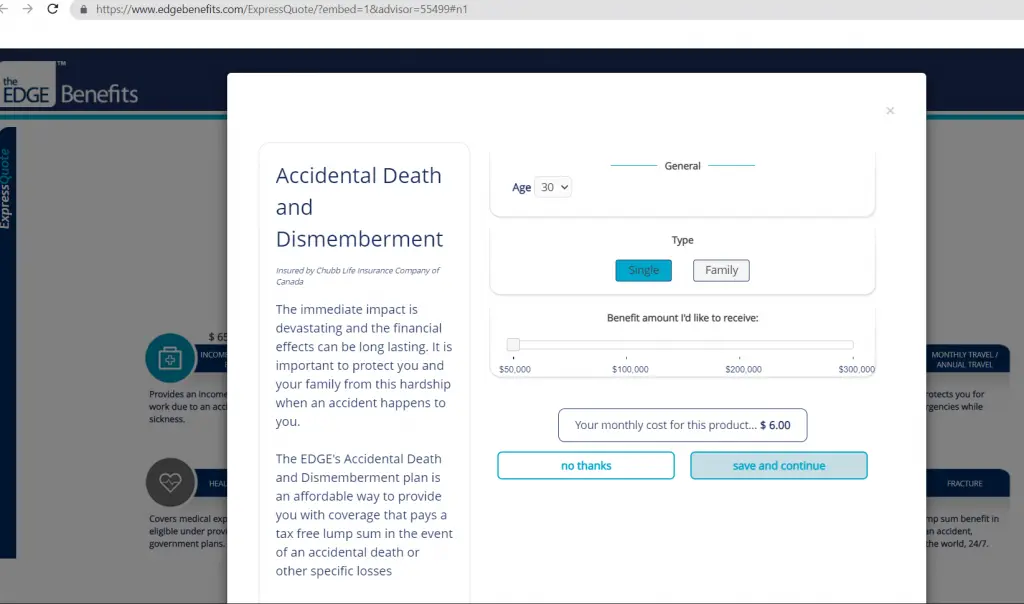

Fill up your details, click “SAVE AND CONTINUE” as shown in picture: age, gender, employment type, income type, annual income, monthly benefit amount you would like to receive and waiting period. Please note that they already set the benefit period to age 70 in the online quote. Select “ACCIDENTAL Select ” ACCIDENTAL DEATH AND DISMEMBERMENT” and select the type and amount you would like to receive in the pop up, and click “save and continue” as shown in the picture.

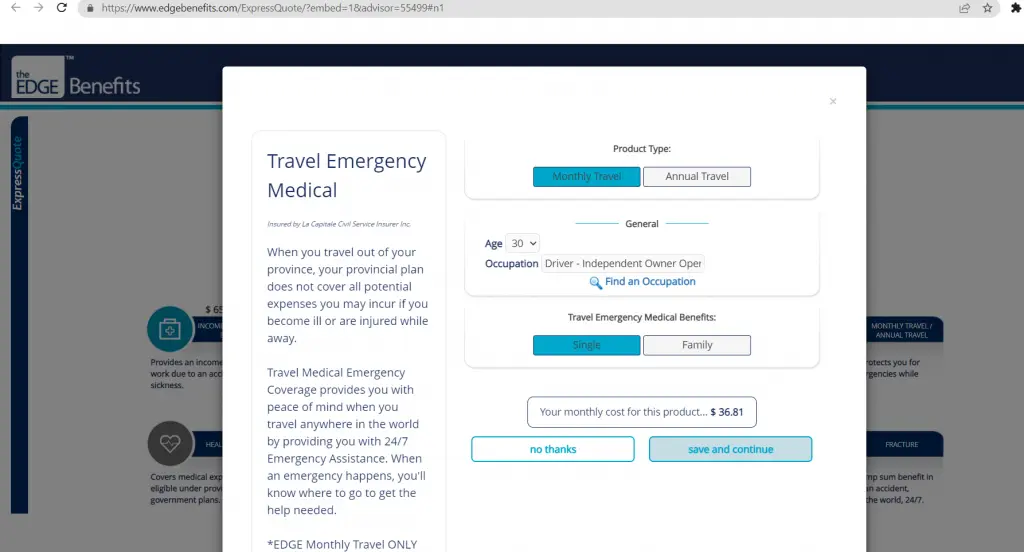

Now click “MONTHLY TRAVEL/ANNUAL TRAVEL” and select monthly travel and single and click “save and continue” as shown in the picture.

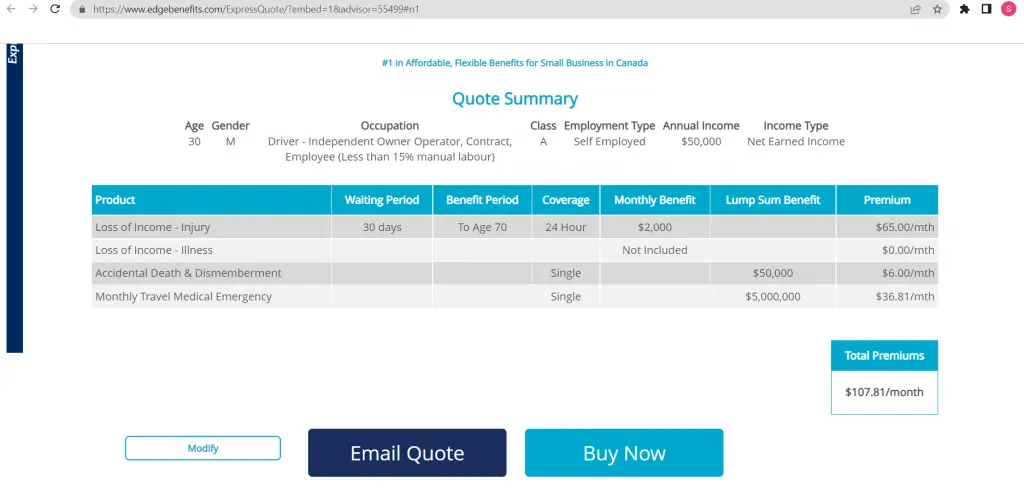

Now on the last screen, click “continue to Summary” and it will redirect you to the last page, as shown in the picture. You have two options: “Email Quote” “Buy Now”, select which one you want, “Buy Now” to complete the purchase or “Email Quote” for detailed information.

Contact us for more information and to prepare an emergency medical insurance plan. Let’s make a plan for you, add a multi life discount and customize it according to your budget and needs. We are available on our social contacts.

How much life insurance do I need? Click here to calculate. Or read the complete article.

What is Life Insurance?

This is an agreement between two parties, the policy owner and the insurer. If the insured dies, the insurer pays the benefit to the beneficiary. An insurance contract or agreement is a written agreement between two parties, where the first party or insurance company assesses the other party or the insured’s financial, health and living conditions and provides life insurance at the request of the applicant.

Highlights

The policy starts when two parties enter an agreement or a legal contract.

In most cases, the insurance policy remains in force until the insured dies, or the last premium, or until the insured surrenders the plan.

As per the contract, the benefit amount may change or stay the same to the maturity.

The insurer’s guarantor pays benefits to the insured in case the insurance company files bankruptcy.

In terms of life planning, life insurance is the most important decision. Mishaps can occur at any stage of life, including birth, marriage, childbirth, and old age. We offer plans that fits every stage of life so that you and your family are prepared.

Why it is required?

There are many reasons for life insurance, such as

Financial protection:- This is the best and cheapest way to secure your financial security, as we mentioned earlier. If you are concerned about the financial future of your loved ones, then you should purchase life insurance to ensure that they can easily pay off your debts, final expenses, and taxes.

Legacy for family:- Buy life insurance to leave a legacy for your family and children. We offer life insurance plans with cash value and investment options.

Tax-free payments:- If you pass your house or property to your children, it will be taxable under the rules, but life insurance benefits are tax free, as long as they named the beneficiary in plan.

Creditor protection:- If they properly drafted the policy, its death benefits and cash values are protected from creditors. If a business owner wants protection against bankruptcy, creditor protection is an important feature.

Living benefit:- If an insured is diagnosed with a terminal illness, the policy can become a living benefit. If you are worried about mortgage, bills, taxes, daily life expenses and legacy for kids, then you need it for sure.

As per BNN Bloomburg, only 38% Canadians have group or individual plans, and one third of Canadians have no coverage. The one third number is big, every life is important.

Types.

Term life insurance

As the name implies, term insurance has a defined duration, such as 10 years, 20 years, 30 years or more. Since it has a fixed duration, term plans are cheaper. Note: We can also use term life insurance as mortgage insurance

Further, the term life insurance can be divided into:

Decreasing Term – The amount of coverage decreases overtime, and our liabilities also start decreasing after a certain age, so term plans are applicable in those cases.

Variable or Convertible Term Life Insurance – The term type allows the insured to switch to permanent insurance at the end of the term.

Renewable Term Life Insurance – The annually renewable policies, where the premium increases every year, being cheaper in the beginning and becoming more expensive as the policy grows.

Permanent life insurance

This policy will last for as long as the policyholder continues to pay the premiums or surrenders the policy. Since it does not have a time limit, it is expensive than term life.

We can further divide the permanent plans to: –

Whole life insurance:- The life policy with a cash value and death benefit are comes under this category. In the other words, it is called money back life insurance policy, in which the insured can access the accumulated fund and keep their policy in force as per contract terms.

Universal Life Insurance:- It is a flexible policy with the investment options and a good amount of coverage. The insurer can deposit higher premiums in the UL policy, those leads to investment and coverage. Some other features for UL plan include flexible payment plan, short-term payment options such as 10, 15, 20 year pay, and higher growth funds. Indexed Universal and Variable Universal are two other types of permanent life plan.

Term VS Permanent Life Insurance

It is inexpensive, comparatively one can buy more coverage with the same amounts.

Temporary coverage from the financial impact of death.

Young families, homeowners with the mortgage, and business loan owners are the buyers.

Convertible to permanent, return of premium options are the key points.- Lifelong coverage from the financial impact of death.

Adults with long life goals, and want to invest in the legacy, are major buyers.

Lifetime coverage, bit more expensive, but comes with better investment and growth opportunities.

Permanent coverage, short term pay off options are the key points.

Now, questions come up to our mind, like how much insurance do you need? How much coverage do I need? How much can I save by investing in the UL policy?

We have answers to all questions, and work with the best life insurance companies such as sunlife, IA, rbc, manulife.

Let’s sit together and plan a perfect solution for you. Our experts are available online and offline as per your convenience.

Why do we need 3 Month Waiting Period Health Insurance?

If you are entering Canada for the first time or have lived outside Canada for 182 days (212 days in Ontario), you must wait 90 days for provincial coverage and probably need 3 Month Waiting Period Health Insurance while waiting for provincial coverage. Which is commonly known as 3 month waiting period insurance.

We got a competitive plan, which will protect you from unexpected expenses and cover your health problems.

If you are a landed immigrant, or Canadian citizen returning to Canada after a long stay in abroad, you will need insurance to see a doctor in an emergency. One option is you can pay out of pocket, but Canadian healthcare system is very expensive, that is why it is hard for a new immigrant to pay the hospital bills.

How much does it costs?

The 3 Month Waiting Period Health Insurance is not that expensive, on an average, it costs around $60/Month, but the hospitalization is expensive, almost impossible to pay out of pocket. You are welcome to check for free how much emergency medical insurance will cost?. This is not only the emergency health insurance quote, it also includes pricing, scope of coverage, policy wording and a link to purchase.

Can I cancel or extend emergency medical insurance?

Yes, our providers are quite flexible, you can cancel with some reasons. Sometimes, you may need to apply for extension also, in health card delayed, or forgot to apply on time.

Can I buy visitor insurance after landing in Canada?

Yes, you can still buy it if you arrived in Canada uninsured, provided you are ready to bear some wait times.

Visitor insurance vs Emergency medical insurance for returning Canadians.

There may be a difference in duration, mostly visitors need longer coverage than returning Canadians. You can get a no obligation quote now and purchase according to your needs.

Provincial healthcare outside your home territory/province.

The provincial health care has some limitations out of the province. Some workers, such as truck drivers, out of province travelers might need an extra layer of protection. Luckily, private health insurance or emergency medical insurance is available to protect us.

For example, if you are in the province of Ontario and need access to emergency medical services, while you are physically present in Manitoba, you can get those services with the insurer.

We have special plans available, such as emergency medical insurance truck drivers, health insurance international students and temporary workers.

Contact us for package deals, or job specific plans.

Unless you are a citizen of a visa-exempt nation, you need a visa to enter Canada as a student, permanent resident, to work or explore Canada. A visitor visa, also called a temporary resident permit (TRV) or 10 year multiple entry visa, allows holders to stay in Canada for 6 months.

What is the difference between tourist visa and visitor visa Canada?

The tourist visa is intended for sightseeing, exploring Canada, while a visitor visa is intended for visiting family members abroad. Visitors may also explore Canada under a visitor visa, but most people apply to meet family members.

What is the difference between tourist visa and visitor visa Canada?

Submit the insurance policy with the super visa application as soon as you receive it. Now that they have approved the visa, your parents will land in Canada, and the next instalments will begin from landing.

If you want to change the date of landing, let us know at least 7 days before the intended date of landing. We will adjust the date and the next monthly payments will start from a new date.

Why is visitor insurance crucial?

Thanks to Canada Immigration, they made the insurance mandatory for super visa applications. We all know Canadian healthcare is the best in the world, but it is expensive. God forbid if an uninsured visitor needs hospitalisation. It is very hard to pay for it. Although travel medical insurance is not compulsory for tourist applications, it is a lifesaving utility.

Visiting or exploring: the trip should be secure and peaceful, is another reason for visitor visa insurance or and travel insurance are vital in all cases.

What happens if a tourist or visitor gets sick in Canada?

The Canadian health system is one of the best in the world, but it is expensive. If you get sick or involved in an accident in Canada, the Canadian government will not pay the medical expenses, you need to pay out of your pocket. As we know health care is expensive in Canada, the hospital bill could be in thousands. The best alternative is health insurance, also called travel insurance or visitor visa insurance.

Good news is you can buy visitor visa insurance online. Click here to get a visitor visa insurance quote or travel insurance quote now.

How much does a doctor’s visit cost to an uninsured?

A doctor’s visit can cost around $150/per visit, whereas the hospital visit could cost in thousands. The visitor insurance is not that expensive and is a worry free solution.

Which is the best health insurance for visitors to Canada?

All Canadian insurance companies offer the best plans. We have coverages available from $10K to $300K to best fit your needs and budget. The best is fit with in your budget and needs. We already did shop around for you and filtered out the best visitor visa insurance companies. Just fill in the form below and buy the best coverage.

What is the cost of visitor visa insurance?

The cost of visitor to Canada health insurance for a 30 day trip with $50,000 coverage with 0 deductible for age 40-45 applicants will be $60 to &90. The following factors determine the cost of visitor to Canada’ health insurance:

Health Status:- The coverage is cheaper for healthy travellers, but expensive for pre-existing health conditions. Age:- It is cheaper for younger ages, as we know the probability of claiming is low in young people. Amount of Coverage:- The cheapest plan is with $10,000, but most people prefer buying a $100,000 plan. Number of visitors:- Some companies offer special discounts to groups, family members and dependents.

Can I work with a visitor visa in Canada?

You need a work permit to work in Canada. You can not work on a visitor visa in Canada. As per Canada immigration, a visitor visa holder can not engage in any commercial activity and enter the labour market in Canada.

How can I convert my visitor visa to a work permit in Canada?

You need a job offer from a Canadian employer to convert your visitor visa to a work permit in Canada. The steps are: –Apply for a job. –Get LMIA. –Apply for a work permit in Canada.

How to apply for a visitor visa to Canada?

You can apply online or offline. For faster processing and accurate filling, it is better to apply online. Click on the following link for accurate information as per the immigration Canada website: Visitor Visa Application.

or contact us to apply through an immigration lawyer.

What are the documents required for a visitor visa application?

Basically, you need a passport, proof of funds to support your stay in Canada, and a letter of invitation from your relative in Canada. Apart from it you might need a use of representative declaration form if you are using a lawyer or representative in the application.

How long does it take to get a visitor visa to Canada?

The processing time for a Canadian visitor visa is 15 days, provided your documentation is accurate. It depends upon your country of citizenship and application.

Can I extend my visitor visa in Canada?

Yes, you can apply for a visitor visa extension. You need to apply at least 30 days before the current status expires. We can help you with the application. There is no statutory limit on the number of times a person can extend the visitor status.

Is the return ticket required for a visitor visa to Canada?

Although it is not a legal requirement, I strongly recommend that you have a return ticket. The officers at the port of entry may ask you for a return ticket.

What is the difference between a visitor’s visa and a visitor’s record?

A visitor visa is a sticker on your passport to enter Canada as a visitor. As per immigration Canada, you must apply from outside of Canada. The visitor record is a document that immigration officers use to extend or restrict your stay in Canada.

We usually receive a visitor’s record when we apply for a visitor visa extension.

Contact us for further visitor visa questions. Or post your question in the comments.

Why is the international student insurance required?

It is wise to purchase medical insurance for your own safety, regardless of whether you are studying abroad or travelling. At first, living away from family abroad can make it difficult to bear the burden of education and to take care of oneself. The second problem is the expensive Canadian health care system, making it very difficult for a student to pay for medical treatment with college fees. Canadian residents are covered by the free health care system, but students and visitors are required to pay; international student insurance or private medical insurance is a suitable alternative.

What is the cost of an international student health insurance plan?

It costs between $600 and $900 for international students to get health insurance in Canada each year. There are many companies offering coverage for around $600 per year, with total coverage of 2 million, and some medical expenses, such as dental treatments, medicines, and physiotherapy, are covered up to a dollar amount.

You can find out the cost of medical insurance for international students by clicking on the link above. International student health insurance plans are also available in group plans. We have the best group policies. Contact us today and start designing a group policy for your students.

Can I get health insurance after getting a student visa?

There is still a chance that you can get insurance even if you arrive here uninsured, but please keep in mind there may be a delay in starting your coverage. If we buy the policy before landing in Canada, there is no waiting period. Read the policy terms and conditions for further information on waiting periods.

Does a Student Insurance Plan Cover Pregnancy?

There are many international student insurance plans that do not cover the normal birth of a child, but do cover complications during pregnancy. In contrast, some companies offer to $10,000 in coverage for childbirth.

If you are an international student and are planning to have a baby, contact us today for adequate insurance. Pregnancy insurance has many limitations related to regular checkups, pregnancy weeks, so before buying, carefully read the terms and conditions. If you buy coverage after pregnancy, it will cover the complications of pregnancy but not the cost of childbirth.

Provincial health care card or health card.

To receive free provincial healthcare services in Canada, you need a health card. Immigrants, work permit holders, and some other status holders may receive health cards from their provincial governments, depending on their eligibility. Do you qualify for a health card? Click the link to find out.

After applying for the first time for OHIP in Ontario, you may have to wait up to three months. After three months, eligible Canadians receive this card, but students cannot apply for it until they have a work permit. As soon as they get a work permit and become eligible, they can get a health card.

How to get a health card?

In each province, we can get health cards from the relevant service providers. In Ontario, for example, one can apply for a health card by showing an acceptable ID.

Do not share your health card with anyone else, because anyone can misuse it and sharing a health card can be a criminal offence. The Provincial Health Card also has further limitations, as it does not cover dental, vision, physiotherapy, prescription medication, etc. A separate health and dental coverage is available for these services. I recommend that all students studying in Canada take out international student insurance, as it is difficult to cover the cost of treatment with tuition and living expenses.

Please share this article on your social media channels.

A coverage for deadly diseases such as cancer, heart attack, major organ transplant, deafness, coronary bypass surgery, etc. is called critical illness insurance.

An insured receives a tax-free benefit from the insurer if diagnosed with a condition. In Canada, almost all insurance companies offer this coverage for 4 to 25 illnesses.

The policy wordings explains coverage, illnesses, and the payout amount, please read carefully before signing.

Is critical illness insurance worth it?

Yes, this is a protection from unexpected illnesses.

The insurer pays a lump-sum benefit to the insured, upon diagnosis of the critical illness listed in the contract.

This coverage is useful for those who don’t have a comprehensive benefit package from the job. It is also crucial for the people who do not have sufficient savings.

According to statcan, about 30% of illness related deaths are because of chronic diseases.

Which diseases does this cover?

They cover almost all deadly diseases, however there may be a rated underwriting for people with health issues. Most insurance companies offer coverage against 4 or 25 illnesses. Read your contract or consult us for expert advice.

The most common 25 Illnesses covered are.

Alzheimer’s disease.

Aortic surgery.

Aplastic anaemia.

Bacterial meningitis.

Benign brain tumour.

Blindness.

Cancer (life-threatening).

Coma.

Coronary artery- bypass surgery.

Deafness.

Heart attack.

Heart valve replacement.

Kidney failure.

Loss of independent existence.

Loss of limbs.

Loss of speech.

Major organ transplant.

Major organ failure on the waiting list.

Motor neuron disease.

Multiple sclerosis.

Occupational HIV infection.

Paralysis.

Parkinson’s disease.

Severe burns.

Stroke (cerebrovascular accident)

Things to keep in mind when buying critical illness insurance.

– Your current financial status. – Health and age. – How much coverage are you buying? – What diseases are you buying for?

We can combine this plan with life insurance. Sometimes, critical illness insurance is available as a package with life insurance for free, which is a great deal. Sign up for our newsletter, and we’ll let you know when it becomes available.

How does it works?

The insurer pays lump-sum benefits to the insured upon diagnosis, depending on the contract.

What is the difference between disability insurance and critical illness insurance?

These two types of insurance cover individuals and groups, where disability insurance covers injury-related loss, and critical illness covers illness-related loss.

Can a sick person get insurance for a serious illness?

It is still possible to apply for the coverage if you have been diagnosed with or treated for a critical illness.

Finally, expert advice is very important, because illness definitions are transforming, and our team is here to help you with up-to-date knowledge and expertise

When you cannot work, disability insurance works for you. Besides being tax free, disability payments help protect your savings when you cannot earn a living.

When buying a disability plan, consider:- Benefit Amount – The monthly amount that can be paid out after a claim is called the benefit amount. Payout Period or Benefit Period – The number of years the disability payments will continue is called the Benefit Period. Waiting Period – The waiting period is usually the time to receive the first payment after making a claim.

How much disability insurance or benefit amount does you need?

We can determine the benefit amount we need based on our expenses, income, and future needs. We need to cover 60 to 80 percent of our income, and can add a total disability payout for the future needs. Plans with the smaller disability benefit amounts are comparatively cheaper. Insurance companies pay based on the taxable income, so buy accordingly. We are here to assist you with your disability insurance needs. We assess your needs and shop around for the best options.

How long is the Disability Benefit Period we need?

Plans are usually available for two years, five years, and up to age 65. The premium of disability insurance depends on the payout period or benefit period, it is cheaper with a short payout period or benefit period.

Although we cannot predict, but we can plan, according to the:-

Risk at job – I will consider long-term disability payout periods if working in a hazardous environment, such as a truck driver or construction worker. A long-term disability payout is more expensive than a short-term disability payout, since it exposed the insurer to a longer-term risk. You must also consider your health and the way you live your daily life, for example, if you cannot exercise and work a sedentary job. According to a survey, 90% of disabilities are because of illnesses, so long-term disability plans are better.

What is the disability waiting period?

Waiting between an incident and the first payout is called the wait period. There are three common waiting periods: 0 days, 30 days, and 112 days. A plan with longer waiting periods is comparatively cheaper. Experts can answer questions about the waiting period, such as why we need minimum waiting periods, when we need longer waiting periods?

What is the cost of disability insurance?

It depends on the following factors.

Coverage Amount – How much coverage you are applying for? It is important to note that you can only receive a disability benefit based on earnings. The duration of benefit – This is also called the benefit period. Which is for how long should disability benefits last, 2 years, 5 years, or until retirement age? Waiting time – When the benefits or disability payments start, after 0, 30 or 112 days. If you have employment insurance, choose 112 days, because EI pays you for 112 days in case of disability claim.

Age – Disability insurance is usually cheaper for younger ages. Health – Disability insurance is cheap for the affluent. Work – Another factor determining disability premium is the nature of your occupation. Risky jobs are more expensive.

How much disability insurance benefits will I get?

A typical insurance company pays up to 80% of your income, so buy it according to your income. The following table shows income and potential benefits. There are some government disability options available, such as CPP and DCPP, but the qualifying criteria are very restrictive, and the maximum benefit is less than $1500.

Riders on Disability Insurance.

A rider is an add-on with the plan, a disability plan can have the following riders.

Waiver of premium – When an event triggers a waiver of premium, the insurer waives the premium. When you are disabled, they stop collecting the premiums. Return of premium – If no claim is filed until the maturity date, the insurer can return the premium. Total disability benefit – The insurer pays an additional benefit in case of total disability.

Disability insurance in a package.

Special packages are available for truckers, construction workers, and other high-risk occupations. We can combine disability insurance with emergency medical coverage for truckers and with sickness coverage for chemical factory workers.

Group disability insurance vs. individual disability insurance

Plan might end when you leave your job – Could be yearly renewable.

Same plan for all members of the group – Individual

Plan will be with you anywhere – Premium remains the same always.

A customised plan according to you – Individual disability insurance premiums remain the same, although most group insurance plans have variable premiums. There is no choice in group disability plans. You must take what the group offers. You can only choose options in an individual plan – Group plans are comparatively cheaper than individual disability insurance plans.

For truckers, we offer insurance packages, such as disability insurance with life insurance or disability insurance with travel insurance. Talk to our advisor today and protect yourself. Disability coverage is available for short-term, long-term, and permanent disabilities.

A term life insurance policy lasts for a fixed period, such as 10, 20, 30 or 40 years. The best thing about term life insurance is the price, but the downside is that you will be uninsured after the term ends.

Life insurance policies end with surrender or maturity, not with death, if the insured outlives the term.

Why do we need it?

An affordable form of life insurance can ensure the financial stability of your loved ones after your death, as well as providing you with a good level of security. It will give your family member (beneficiary) a lump sum tax-free benefit they can use for paying taxes, mortgages, loans, and other debts. We can help you determine your term life insurance needs and provide you with the most appropriate policy.

Term Life Insurance vs Permanent Life Insurance.

Coverage for defined period – Comparatively cheaper.

Nowadays, no money back rider is available in term plans – Convertible to permanent and renewable as term plan.

Amount of coverage may decrease over time or can stay level – Coverage for life.

Expensive than permanent coverage – Money back, cash value and investment options.

It is already for whole life, so no need to renew or convert. Coverage may remain the same or increase as per contract.

Types of Term Life Insurance.

There are multiple types of plans, even though it appears to be one.

Annually renewable term:- In the beginning, the premium is lower, but it increases as you get older. Renewable terms are convenient for managing budgets, and if we calculate the total premiums, it is almost similar to level terms.

Decreasing benefit term:- The benefit amount decreases over time. So these plans are an excellent alternative to mortgage insurance, credit coverage, and loans.

Convertible to permanent: – If you change your mind, even after up to five years, you can convert to permanent life insurance. Some vendors carry forward your paid premiums, as per policy provisions. We have excellent offers on such plans.

Riders on term life insurance.

Riders are additions to the policy. In the other words, we can bundle some benefits with the plan. Some most important term life insurance riders are:-

Waiver of premium:- In case an insured of the policyholder becomes disabled, this rider waives the premiums. A waiver of premium rider is available to both policy owners and insureds. Please read the terms and conditions carefully.

Guaranteed insurability rider:- This rider allows you to purchase additional coverage without further medical questions. This rider is useful in all life events, such as marriage, birth of your child, change in your income, and ageing.

Accidental death rider:- This is very useful for breadwinners. It can double the death benefit in case the insured dies in an accident. This rider is the best choice for those working in accident-prone environments, such as truck drivers, construction workers, or those working in mining or heavy metal processing.

More Riders.

Family income benefit rider:- In the event of the death of the insured, the family would receive a steady income stream.

Accelerated death benefit rider:- Upon diagnosis of a terminal illness, the insurer may pay a living benefit amount.

Child term rider:- This rider offers great coverage for the entire family. If a child passes away before a certain age, the insurer will pay the death benefit. Otherwise, they can convert to a permanent plan, as specified in the terms and conditions.

The return of premium rider is almost no longer available; however, some insurers still offer term life insurance with the return of premium. Upon maturity, the insurer returns the whole or partial primum.

Long-term care rider:- The insurance company can pay a monthly benefit if the insured has to remain in long-term care or receive LTC at home.

Do you need term life insurance? Click here to buy now. Talk to us today and protect yourself.

Now, it opens up in a new browser(make sure pop-ups are not blocked). Click on the “INCOME REPLACEMENT BENEFITS” as pointed in the picture.

Now, it opens up in a new browser(make sure pop-ups are not blocked). Click on the “INCOME REPLACEMENT BENEFITS” as pointed in the picture.

Select “ACCIDENTAL Select ” ACCIDENTAL DEATH AND DISMEMBERMENT” and select the type and amount you would like to receive in the pop up, and click “save and continue” as shown in the picture.

Select “ACCIDENTAL Select ” ACCIDENTAL DEATH AND DISMEMBERMENT” and select the type and amount you would like to receive in the pop up, and click “save and continue” as shown in the picture.